Executive Summary

One of the hardest risks to manage in retirement is the uncertainty of longevity – how long the retiree will live, and therefore how long of a retirement time horizon needs to be planned for. Planning for too short of a retirement time horizon can lead to asset depletion if the retiree actually lives. Planning for too long leads the retiree to unnecessarily constrain retirement spending for a future that never occurs.

While one popular approach to managing the issue is simply to invest in a diversified portfolio, spend conservatively, and make adjustments in the future as necessary, an alternative is to actually buy “longevity insurance” in the form of a lifetime annuity. Historically, this could be done by purchasing a single premium immediate annuity at retirement, except in practice retirees rarely ever want to lock up so much of their capital - in fact, retirees annuitize so rarely that economists have dubbed it an "annuity puzzle".

A potential alternative, though, is to use a longevity annuity. This form of single premium deferred annuity still provides payments for life, but with payouts from the longevity annuity company not beginning until the distant future (e.g., at age 85). The upshot to this approach is that it significantly reduces how much capital must be committed to securing the longevity insurance guarantee, even as the deferred starting date can also delay required minimum distribution (RMD) obligations if purchased as a "qualified longevity annuity contract" (QLAC) inside of a retirement account.

And despite today’s low interest rates, a current longevity annuity quote reveals that it can already be an appealing competitor to the expected returns of a fixed income portfolio. In fact, if longevity insurance rates rise just a bit more, they may even become competitive with long-term equity returns, thanks to the benefit of mortality credits. Which means eventually, an allocation to a “longevity annuity bucket” may become a standard in retirement income planning… at least, as long as life expectancies don’t increase so much in the coming years that the longevity annuity rates just end out going down!

Retirement And Longevity - The Unknown Time Horizon Problem

One of the greatest challenges to crafting a retirement portfolio and retirement spending strategy is that both are highly dependent on a completely unknown variable: the time horizon for retirement itself. After all, those who will live in retirement for “only” 10 years can spend far more than those who may be retired for 30+ years, and the latter also may need a larger allocation to growth investments to keep up with the pernicious impact of inflation compounded for decades. Yet without knowing the time horizon, it’s impossible to know whether spending should be higher or lower, and whether the portfolio can be more conservatively invested or “needs” to be somewhat more aggressive.

In the extreme, one approach to handling the situation is simply to put most or all of one’s retirement funds into an immediate annuity, which eliminates the time horizon problem for the retiree by receiving guaranteed payments “for life” from the insurance company. Technically, this simply shifts the unknown time horizon from the individual to the insurance company, but the good news is that thanks to the law of large numbers the insurance company can predict the time horizon for a large group of people with a relatively high degree of accuracy – far more than any one retiree can for just their individual sample size of one.

Yet the caveat to the immediate annuity solution is that, despite its simple elegance, virtually no retirees actually annuitize a significant portion (much less all) of their retirement wealth. One research study found that immediate annuities would leave most retirees ill prepared for a health care “shock” event (except, ironically, those who have so much money they wouldn’t need the annuity anyway). Some theorize that in general retirees just have a stronger preference for liquidity than what an immediate annuity offers. Others suggest it’s simply because the payouts are too low.

Yet whatever the reason, this “annuity puzzle” persists, and retirees who “could” solve the time horizon problem by annuitizing most of their wealth continue not to do so.

What Is Longevity Insurance And How Does It Manage The Retirement Time Horizon Problem

Longevity insurance, also known as a longevity annuity or an advanced life deferred annuity, is a form of deferred annuity contract designed to provide “payments for life” but with payments that don’t begin until the distant future. Thus, for instance, while a single premium immediate annuity would provide lifetime income beginning now (e.g., purchased at age 65 with payments beginning at 65), the longevity annuity would take the same lump sum up front (at 65) but payments might not begin until the distant future (e.g., age 85).

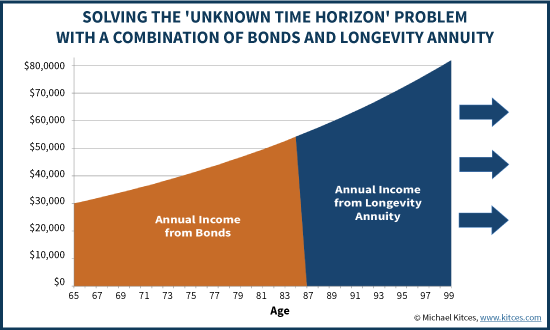

The benefit of using longevity insurance as part of a retirement portfolio is that it helps to solve the unknown time horizon problem. For instance, imagine a 65-year-old couple that purchases a longevity annuity that will begin to make significant payments at age 85 to cover all their (inflation-adjusted) needs later in life. This couple’s retirement investment puzzle is now greatly simplified: they just need to cover the fixed time horizon of the next 20 years, because the longevity annuity will take care of “everything thereafter” if they are still alive.

In other words, the couple has just turned one of the biggest retirement challenges – investing for an unknown retirement time horizon due to the uncertainty of mortality/longevity – into a much more manageable problem over a known time horizon of investing from the start of retirement until the annuity starting date when the longevity annuity payments kick in. From that point forward, the longevity annuity covers “everything”, regardless of how long the retiree lives. In essence, the longevity annuity is providing longevity insurance against the retirement portfolio and creates an “end point” (when the longevity annuity payments begin) that most retirement plans don’t have when the retiree otherwise doesn’t know how long he/she will live.

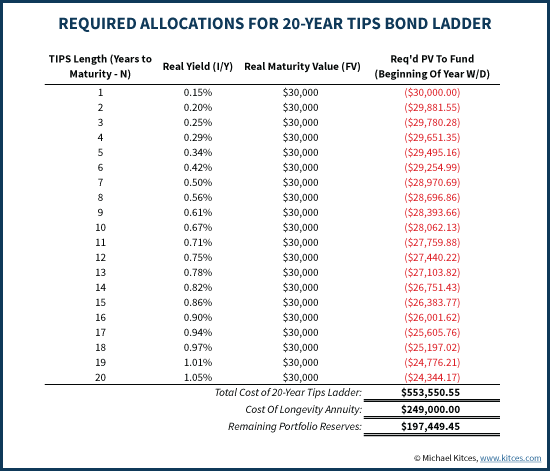

Thus, continuing the prior example, let’s assume this 65-year-old couple has $1,000,000, and wants to spend $30,000/year from their portfolio (adjusted for inflation) for the rest of their lives, to supplement available Social Security income. At 3% inflation, $30,000/year will be $54,183/year in 20 years (at their age 85). Based on current pricing (for inflation-adjusted payments, with a joint survivorship payout that continues as long as either are alive, and a cash refund guarantee), this couple can buy a longevity annuity for their future $54,183/year (which is $4,515.28/month) beginning at age 85 for a longevity annuity cost of about $249,000. This purchase will leave the remaining $751,000 of the portfolio available to cover just the next 20 years.

Now, instead of trying to invest $1,000,000 for a $30,000/year inflation-adjusted income for an unknown time horizon, the couple can invest $751,000 for a $30,000/year inflation-adjusted income for exactly 20 years, secure in knowing that all payments beyond that point will be covered by the longevity annuity and backed by the longevity insurance company.

Using A TIPS Bond Ladder To Secure 20 Years Of Inflation-Adjusted Retirement Income

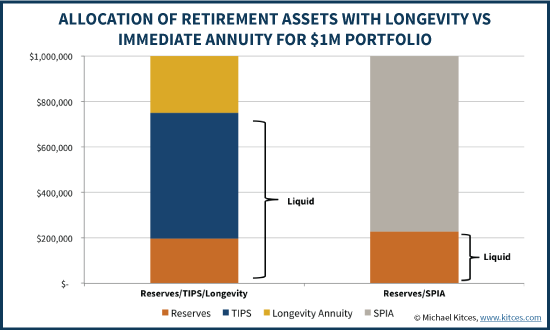

Once a longevity insurance ensures that the later years are covered, the initial 20-year time period of a retirement portfolio could then be covered with a diversified portfolio, or simply by something like a ladder of TIPS bonds, providing the exact amount of inflation-adjusted income for each of the 20 years, and entirely securing the couple’s lifetime income! In fact, it would only take about $554,000 to buy a ladder of TIPS to cover the payments for the next 20 years, leaving almost $197,000 left over as well! And whether the couple lives to age 85, 95, or 105, they will have inflation-adjusted income for life as the longevity annuity payouts occur in the later years.

Of course, the reality is that this 65-year-old couple could have simply purchased a single premium immediate annuity with inflation-adjusting payments to cover their lifetime guaranteed income goal as well, simply starting at age 65 when they retired. However, the purchase of an immediate annuity (again inflation-adjusting, joint survivorship payments, with a cash refund guarantee) would require about $772,000 of their capital, leaving only $228,000 over for ‘emergencies’ and contingencies – which is similar to the $197,000 left over from the longevity annuity scenario. Except remember that the $554,000 in TIPS bonds would still be a liquid portfolio that could be adjusted if desired!

While it may be appealing to use the longevity annuity in this context, as it obtains similar longevity guarantees but at a lower upfront cost, it’s notable that the total “cost” in required dollars is similar. This shouldn’t be surprising, as whether buying a TIPS portfolio plus an inflation-adjusted longevity annuity, or an inflation-adjusted immediate annuity to cover the same time period, both the investor and the insurance company are ultimately investing in the same capital markets for the same time horizon and the same available bond yields! The only difference is the liquidity of the capital in the meantime, which arguably would be more appealing in the longevity annuity scenario over the single premium immediate annuity (similar income, similar costs, and more liquidity in the meantime).

[Tweet "Longevity annuities have better liquidity than immediate annuities with similar lifetime guarantees!"]

Longevity Annuity Rates Versus Long-Term Equity Returns

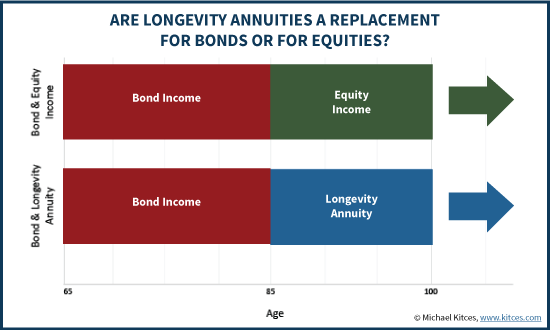

In a world where the longevity insurance covers retirement spending for those who live past an advanced age like 85, the portfolio design process is greatly simplified; it just needs to cover the finite time period from retirement (e.g., age 65) until the payments begin from the longevity annuity. This 20-year time horizon would likely be covered by a rather bond-heavy portfolio (given how much spending must be supported in the near- and intermediate-term years) and as noted earlier might even be funded outright with a 20-year (TIPS) bond ladder.

In turn, this means that in practice, the longevity annuity is likely to replace primarily equities in the portfolio, which are what would have been otherwise invested for retirement spending that by definition wouldn’t have to begin for at least 20 years. After all, the reality is that any investor in a simple diversified portfolio could always choose to segment their portfolio into two buckets: one to cover the next 20 years, and one to cover all retirement expenses beyond that point (i.e., age 85 and beyond). At that point, it’s just a question of whether the later-years’ bucket is filled with income from equities, or funded with the backing of a longevity insurance company.

Accordingly, this means an assessment of whether a longevity annuity fits in a retirement portfolios is really a matter of comparing the long-term economic value – i.e., the internal rate of return – that can be produced by equities, versus ongoing cash flows from a longevity annuity.

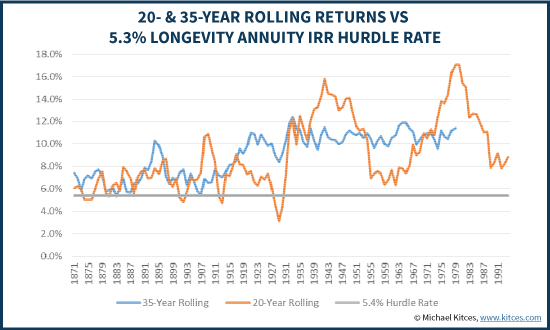

In other words, based on the longevity annuity quote earlier – with a payment for a married couple of $$4,515.28/month – will pay out the equivalent of a 5.3% internal rate of return if at least one member of the couple lives to age 100 (and assuming 3% inflation). Which means to produce equal-or-better cash flows from equities, a long-term equity portfolio must produce a comparable long-term rate of return.

Yet when compared to actual historical returns, suddenly the longevity annuity begins to look somewhat less appealing. The graphic below shows the rolling 20-year and 35-year total return for equities over the past nearly-150 years (based on available data from Shiller). And as the data reveals, it’s only happened a few times in history that equities failed to generate the required 5.3% “hurdle rate” to beat a longevity annuity, even over “just” the 20-year time period from age 65 to 85… and equities have always generated enough return over a 35-year time period (from age 65 to 100) to beat the cash-on-cash payouts from a longevity annuity and still have money left over.

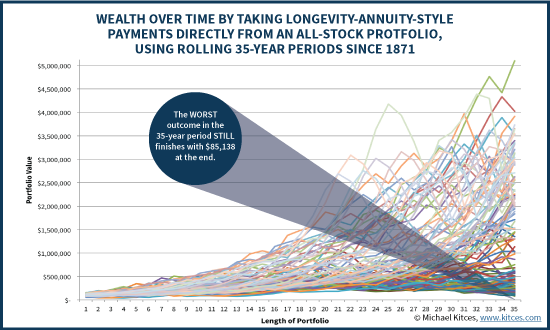

In fact, the graphic below shows the results of simply investing $100,000 in an all-stock portfolio and taking the exact same withdrawals that a level longevity annuity would have paid. At current rates, a $100,000 deposit for a 65-year-old couple would pay $2,255.02/month starting at age 85 (with a cash refund guarantee if the couple dies before all principal has been returned). Yet as the results reveal, even in the worst case scenario the equity portfolio doesn’t run out of money by making the exact same payments as the longevity annuity. In fact, the worst scenario still has almost all the starting principal left over! On the other hand, in nearly half the scenarios, the retiree with equities covers all the payments a longevity annuity would have provided, and has more than 10X their starting $100,000 principal left over as well (i.e., starting principal grows over $1,000,000 in value, on top of funding all longevity annuity withdrawals!). In some cases, starting principal is multiplied by 20X, 30X, or even 50X!

What this dichotomy highlights is that, for most retirement scenarios, the real challenge point is not necessarily getting sufficient returns to fund retirement with growth in the later years, after the first 20 have already passed (e.g., with a longevity annuity, or just with equity investing); it’s generating enough of a return to fund the first half of retirement without using up all the available assets (given the lower returns entailed in investing for the shorter portion of the time frame!).

In other words, to the extent that cash flows can be addressed sufficiently to cover the first half of retirement, the time horizon is long enough that an equity-centric portfolio can fund the “long-term” spending needed in later retirement (for the subset of retirees who even live long enough to need it) without using a longevity annuity. Sequence of return risk isn't an issue for a retiree who's already committed to not touch this portion of funds for 20 years (whether in a longevity annuity or an equity portfolio).

[Tweet "Longevity annuities still can't keep up with the power of long-term compounding equity returns."]

In point of fact, this is also an indicator of why recent research on a “rising equity glidepath” in retirement may be helpful as well; in the few scenarios where equity returns are relatively poor early on (close to the hurdle rate), spending disproportionately from fixed income in the early years and allowing equities to grow – which indirectly shifts the overall portfolio allocation to an increasing equity exposure – actually helps to facilitate long-term success by allowing equities the time to generate the needed returns for later retirement!

Payouts At Current Longevity Insurance Rates Versus A Fixed Income (Bond Or CD) Portfolio

Notwithstanding the implied ‘dominance’ of equities over a longevity annuity in the long run – at least at today’s payout rates – it’s notable that for those who are going to invest purely in fixed income for retirement (e.g., bonds and CDs but not equities), using longevity insurance is still far superior to a fixed income portfolio in the long run.

The primary reason for this is that while a bond portfolio can provide principal and interest payments over time, a longevity annuity provides principal, interest, and mortality credits attributable to all those who didn’t survive as long. In other words, not only does longevity insurance eliminate the time horizon problem for those who live a very long time, but it gives “outsized” payments to those who are the survivors (who receive allocates of principal and interest from the share of those who died earlier).

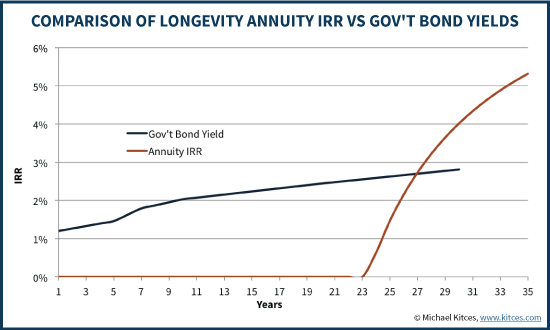

Accordingly, the chart below shows the real (inflation-adjusted) internal rate of return for a longevity annuity from a high-quality longevity insurance company (which in turn is backed by a state annuity guaranty fund) assuming 3% inflation, versus buying the real yield of a government TIPS bond of varying term. In the early years, the government bond is not surprisingly the superior strategy – after all, it doesn’t “pay” to buy a longevity annuity and not live long enough to receive many (or any) of the payments. However in the long run, it’s ultimately the longevity annuity that provides a far superior rate of return.

It’s also worth noting again that this distinction isn’t because the longevity annuity company is a “super investor”, but simply because the company can buy the same bonds as the investor and then stacks mortality credits on top. In addition, from the perspective of time horizon, the longevity annuity is even “more” superior here, because a 30-year laddered bond portfolio runs out in the 31st year, while a longevity annuity just continues to pay, even for those few who happen to live far beyond. In other words, in the long run the longevity annuity both provides a superior internal rate of return for those who live a long time, and gets better for those who continue to keep living – as opposed to a fixed income portfolio, that can run out altogether for those who continue to keep living!

The Benefit Of Longevity Insurance Depends On What It’s Compared To

Ultimately, what all of this really means is that the benefit or “value” of buying longevity insurance in the form of a longevity annuity depends heavily on what it is compared to. Relative to an equity portfolio, the longevity annuity is arguably still inferior, at least given today’s payout rates. In fact, equities so dominate the value of a longevity annuity, that it doesn’t even pay to use a qualified longevity annuity contract (QLAC) instead of an IRA to defer required minimum distribution (RMD) obligations, if it means giving up access to equity returns.

On the other hand, relative to fixed income returns, it is the longevity annuity that dominates, both in terms of returns and the management of the unknown retirement time horizon – and in such scenarios, the potential of a QLAC to defer RMD obligations is just an additional bonus. In other words, if a longevity annuity will be used to replace a fixed income investment and is otherwise appealing, it’s even better to do so with available dollars in a retirement account as a QLAC.

[Tweet "Longevity annuities can be a compelling fixed income alternative for retirees."]

An additional benefit of using this form of single premium deferred annuity is that it provides guaranteed payments for life – similar to a single premium immediate annuity – but the fact that longevity annuity payments only occur for a limited (later) number of means the retiree can commit far less in portfolio assets to get the guarantee. This doesn’t necessarily make retirement “less expensive” in terms of the required assets to support it, but does allow the retirement portfolio to remain more liquid even while securing a longevity insurance guarantee.

In the coming years, though, the real question is whether or how longevity annuity rates will rise (or not) as the Federal Reserve raises interest rates. While interest rate increases in general should boost payout rates, the real impact will be driven by interest rate changes at the long end of the yield curve, not necessarily what the Fed does with short-term rates. And offsetting any benefits of interest rate increases are the “risk” that continued medical advances improve life expectancy so far that longevity insurance rates must actually be decreased instead (to account for longer retirement time horizons of extended life expectancy).

Nonetheless, the possibility remains that in the future, longevity annuity rates may eventually become competitive with or even dominate equities – thanks to the boost of mortality credits – in the same manner that the longevity annuity can already dominate a purely fixed income portfolio for generating retirement income. And at a minimum, the longevity annuity is still the only solution that can take the risk of uncertain longevity and an unknown time horizon off the table altogether. At least, as long as the longevity insurance companies themselves are effective at managing the risk!

So what do you think? Do you incorporate single premium immediate annuities into your retirement plans now? Would you consider using a single premium deferred annuity as a way to provide longevity insurance for a retirement portfolio at a lower cost? How high would longevity annuity rates have to rise for this to be a compelling solution for your clients?

This was interesting and useful. I tried to do this same thing a couple years ago. I wanted to convert an uncertain retirement plan (with respect to longevity anyway) into one that was more crisply defined so that I could try to spend more in retirement without worrying about future “ruin” effects all the time. It was for all the reasons you describe. I did the same process (except that I used a hypothetical 50k in current dollars vs. 30k and designed to cover age 85-100 with age 85 starting in 27 years vs. 20; inflation at 3%; discount at 5%). That meant I had at least a stab at what portion of current capital assets might cover a future “income liability” and the math was not all that difficult. The idea was to then convert some or all of this into a longevity insurance deal. My problem, though, was that, unlike your article, at the time I did this some time around 2012 or 2013 I found that it was hard for me to get a simple quote on a DIA from a couple of the ‘usual suspect’ companies. I couldn’t get a simple one number answer like you got: e.g., “this couple can buy a longevity annuity for their future $54,183/year (which is $4,515.28/month) beginning at age 85 for a longevity annuity cost of about $249,000.” Any advice for getting a transparent price like that? Maybe they are better at it now. Or maybe I was asking the wrong providers.

wks,

It can be done…take a look. “this couple both age 58 can buy a longevity annuity for their future $54,183/year (which is $4,515.28/month) beginning at age 85 for a longevity annuity cash refund cost of $203,425 today. $54,183/year at age 85 will also increase annually at 3%. Joint life only with 3% annual increase after age 85,is only $189,114 deposit today. Hope this helps.

$189,114 invested at a 4% rate of return gets you $613,371 (by the way, the worst 30 year return for a 60/40 balanced portfolio is 6.28%). Sticking the $613,371 under a mattress and pulling out $54,183/year adjusted for 3% inflation takes you to 95 years of age. Longevity annuities are suckers bets sold on fear.

Are taxable bonds paying 4% today? No of course not.

What is MM cash paying today? Next to zero?

And based upon current Shiller CAPE, 4% equity returns over the next decade may appear absurdly ambitious.

After fees, expenses and income taxes, and possible advisory fees as well, what pre-tax return would be required to net your seemingly easy 4%?

7%? 8%? More?

What are tax free muni’s paying you today? Certainly not 4%, maybe half?

What has been the S&P 500 total return over the past fifteen years now since January 1st, 2000? 4%?

No one can purchase the raw Index, you must pay something for it. And net of taxes too? Maybe 3.5%?

So maximum equity market exposure and risk contrasted to the safety and security of the annuity income? You’re comparing asset apples and avocados.

And do you expect to be managing your portfolio when you are age 85 or age 90 and age 95? Really? Or will your wife be forced to “manage” it for you at that time? Really?

In contrast, why not select a deferred income annuity today, which not only pays and credits 3.75%, but also allows for increased income/return as interest rates rise in the years and decades ahead, and fully participates via annual dividends to increase total income and thus your return?

Which is why you would REPLACE the bond element of the suggested 60/40 balanced portfolio you offer, with a lifetime annuity income, which will keep paying, even if you, or your wife lives to age 100, or 105, or 110 etc. And you also won’t be forced to manage your annuity as an elderly and perhaps senile old man, because the income stream will be on auto-pilot.

I question the numbers used in the longevity quote. Are these numbers in today’s dollars or in 2043 dollars when the couple will turn 85? It is my understanding that the inflation adjustments only kick in when the payouts start…is this true? Also, if the “inflation adjustment” is simply a 3% annual increase, then there is really no true inflation protection at all.

2043 dollars or when the income starts. You can also “calculate” what those inflated 2043 dollars should be and then figure out what that deposit would require today. Some carriers have CPI-U inflation adjustments at income start date.

But there is no accurate way to “calculate” what the inflated dollars should be at time of purchase…best one could do is take a wild guess at future inflation rates. Not nearly as much “certainty” as the article implies.

Mike,

Let’s just start and end with the fact that currently longevity annuities are a suckers bet in terms of pricing.

Let’s use your numbers:

I start with $250k. I grow it at only 4% a year for 20 years. That is $547,780 after 20 years.

$54,183/$547,780 is a future payout rate of 9.89%.

By comparison, I could just hold that $250k for 20 years and now have $547,780 of which ***I could buy an SPIA at age 85 and get $63,933.36 or a 11.7% payout rate**. And that is using today’s super low interest rates (and probably would be a much higher payout rate if rates normalized).

Where is all of this additional mortality leverage between age 65 and age 85? I probably have a 30-40% chance of dying and not getting $1, but yet I’m not able to even get a higher total payout rate if I do live??? What possible analysis could have this making sense?

This not hard math or analysis to do Michael. I could have saved you 30 paragraphs.

One day these things might be priced right, but for the time being they’re kind of a joke.

**Admittedly there is a small difference in that SPIA quote I provided wasn’t inflation adjusted as well, but at age 85 there isn’t many years left to have inflation adjusted.

That $54,183 per year should only cost less than $180k (probably ~$160k) if my mortality risk is 33% between age 65 and age 85 (and that is being conservative).

Any insurance carrier that isn’t right now looking at getting into this business is missing the boat because those doing these are effectively minting money on these contracts.

Jon,

A longevity annuity (life only) 65 yr old, $250,000 deposit with payments @ 85 currently is $122,602/yr compared to your $54,183/ yr at age 85 with a SPIA and 4% stock returns above. If you take the Life only part out and include a reduced income payment of cash refund you still get $86,712/yr which beats $54,183/yr! You might want to check out some rates of all the longevity carriers.

I realize this isn’t a question for you, but where is Mike getting his quotes from then?

The few posts I’ve seen from him and others have featured much lower implied payout rates than this.

If those are accurate quotes than now we’re talking.

Mike can you speak to the difference in rates mentioned? This isn’t a small difference in annual income. LongevityInsurance here just provided a quote that was more than double the size of the example in your analysis.

This is a MetLife GIB quote ran today . My sites are http://www.QLACs.net & http://www.LongevityInsurance.com if you need to contact me for anything.

The reality is, compared to bonds within a retirement portfolio, the lifetime income provided by the annuity wins-because it also provides longevity credits (additional income) which no other asset can replicate.

From your prior research, as long as the client is taking 4% or less from the portfolio a longevity annuity is not necessary and most likely will simply result in a huge opportunity cost.

Funny, no insurance company has every marketed this to me for my clients… isn’t that strange. I’d love to learn about them and use them.

To be fair, the products are relatively new, and haven’t been marketed widely at all yet. Though it rates get higher and even more competitive… expect to hear more companies approaching you about them (I hope!).

So far, most longevity annuity sales have been through the captive agent sales forces of the companies offering them (e.g., New York Life’s longevity annuity sold by NY Life agents).

– Michael

Thanks!

Michael, this is awesome.

Thanks Alvin!

– Michael

Another great article! What software or service to do you use to produce you charts and graphs? Are you simply using excel?

We build the charts initially in Excel, but I have a separate graphic designer who gives them a once-over in Adobe Illustrator to upgrade the production quality a bit. 🙂

– Michael

“One research study found that immediate annuities would leave most retirees ill prepared for a health care “shock” event.”

Doesn’t that research explain the aversion to annuities? I struggle to quantify how much I need to reserve for end-of-life and long-term care expenses for DW and myself, and we have LTC insurance.

I am not sure I would recommend for my clients to buy an inflation adjusted annuity, which would sap some of the liquidity from my clients money. Nor would I recommend buying a longevity annuity based on inflating the longevity annuities by 3% a year. Why? I very much question the impact of inflation—other than health care expenses—for people in their 60s, 70s and 80s+.

These people are somewhat immune to inflation (other than health care expenses) because they tend to not buy a lot, but when they do, they shop around. After all, they have time on their hands! In fact their new “job” is to see how little they can spend on things!

How? The aren’t impulse buyers, so they are willing to wait for a sale. And let’s face it: many have pretty much everything they need. What do they really have to replace? In fact they rarely replace their cars (unless they want to) because they don’t drive that far. And by the time they are in their mid-70s, spending on entertainment has gone down.

The kids are out of the house by the time they retire (hopefully) so they don’t really have to buy anything except the essentials. In fact, other than health care, I would say they have more control on inflation than inflation has on them.

So why tie up so much money with an inflation adjusted annuity? In fact, it may make sense to have two annuities: one for essential living expenses (no inflation adjustment), and another for healthcare expenses that is inflation adjusted.

But don’t take my word for it, look at the latest Bureau of Labor 2014 Consumer Expenditure table. There you’ll see that the average annual expenditures for those age 75+ are significantly lower than those in the ages 65-74. And the 65 -74 average annual expenditures is a lot lower than the 55-64 age group. Go to: http://www.bls.gov/cex/#tables_long

I like my clients to use their stock portfolio investments for inflation adjustments in retirement. A longevity annuity (guaranteed income) should at LEAST cover their basic expenses in retirement.

Longevity…I agree, but what I am saying is not to buy an inflation-adjusted amount of longevity insurance (COLA), except for the portion estimated for future healthcare expenses.

So to keep things simple, buy two longevity policies: One without a COLA, which covers future essential living expenses excluding healthcare, and one policy with a COLA for future healthcare expenses. Having two policies also reduces the risk that one insurance might not be able to fully meet its obligations.

Meanwhile, for the “active retirement period,” i.e. before longevity insurance starts, dedicate enough annuity type investments to cover essential living expenses, e.g. Social Security, rental property, pension, and/or annuities. With the remaining money, invest in an appropriate stock/bond/cash allocation to cover the “wants” and “wishes” for clients.

So if necessary (just like with longevity annuities), two income annuities could be used to fill any basic living expense gaps during the active retirement period: One for essential expenses (excluding healthcare), no COLA; and one for healthcare expenses, with a COLA.

Any advisor who places an annuity with a carrier possessing less than AAA, aaa financial ratings is exposing his/her client to credit risk, plain and simple. And preferably a AAA rated mutual carrier not exposed to the whims of market speculation and bloc policies sales to a different stock carrier possessing less than sterling financial ratings. Modest annuity contract values falling within State Guaranty Fund protection limits would seem the only plausible credit excuse.

I understand that this criteria may seem a high hurdle for many advisors, however if we are talking a promise to pay longevity payments 20-30-40 years into the future? We can demand nothing less for our clients, than an impeccable carrier financial profile today. Why settle for less? I certainly would not, nor should my clients.

How true. We as advisors need to put ourselves in our clients shoes, i.e. base our recommendations as if they were for our own well being.

I would like to see that BLS Consumer Expenditure table for people with the $1 million in financial assets that many of our clients have. Most folks are just getting by, and fear causes them to cut back … not so for clients of fiduciary advisors. I’ve not noticed any decrease in expenditures for my older clients.over my 34 years in the biz.

Lifetime annuity income (replacing bonds) in combination with a robust equity portfolio, is typically an optimal risk tolerance allocation of assets for the vast majority of retirees-who expect to enjoy good healthy into their 80 and beyond. This is my observation after 38 years of retirement planning.

BOOM! Drop the mic!

Sagacious messaging needs to be heard!

I believe the only real question is do I start at 80 or 85. If a client has a portfolio that will do well for 20 years then the QLAC is a good diversifier. And yes we want greater guaranteed returns but with 30 year treasuries this low that is a stretch. Coincidentally the IRR at 80 v 85 is pretty similar till you hit 92.(Surprisingly easy to do IRR function on Excel spreadsheet to compare).

In theory I suspect we’ll find the strongest longevity annuity ‘leverage’ is actually to delay even FURTHER, such as to age 90. I’ll be doing a follow-up article at some point to delve into that further and try to tighten up the numbers and how that really shapes up…

– Michael

Theoretically yes. But “real world ” client is the one who ran the numbers and said “I thought the IRR would have been a lot better at 85 than 80” and went with 80. He chose single life with no refund too.

My only problem with this article is the assumption that investors earn S&P returns with the equity portion their portfolio. Investors don’t earn S&P like returns. They experience much lower returns as illustrated by the Dalbar QAIB study, and probably much lower even with the help of a financial advisor. Taking this into consideration, the longevity annuiy is likely superior to retail equity returns over long time horizons.

Good observation and reminder.

The DALBAR study has severe methodological flaws. See https://qa.kitces.com/blog/does-the-dalbar-study-grossly-overstate-the-behavior-gap-guest-post/

That aside, this article is primarily for advisors and the strategies they employ with their clients. Ostensibly the involvement of the advisor is cutting that behavior gap down by keeping clients invested in the first place…

– Michael

I’m sure one can find methodological flaws with any statistical study whether it’s MPT, EMH, Black Scholes, CAPM, …etc. My point is retail investors have two big behavioral problems to overcome that prevents them from acheiving Market returns, which makes longevity annuities a superior financial choice for most. Investors own behavior is the first problem and whether it’s the Dalbar study used as evidence, or tracking retail equity fund flows over the last twenty years (you can get this info from FactSet, Inc if you subscribe), retail investors aren’t pschological up to buying low and selling high, or simply buying and holding. Secondly, financial services is designed to prevent investors from being good investors since the industry must make retail clients churn their portfolios, usually at the worst possible times, to maintain their existence–that is probably why the are fighting the fiduciary rule to vehemently. Investors don’t acheive S&P returns, therefore, longevity annuities are likely superior to retail equity returns over long periods. P.S. I am not a licensed insurance agent, nor do I have a series 7 or 6. I don’t have any skin in recommending annuities for investors.

Daniel,

You are criticizing the role of financial products salespeople.

The readership of this blog are fiduciary advisors. Not only are they not paid to churn and have no need or motivation to churn, but if they did they would be legally liable for it as a breach of fiduciary duty.

I’m not trying to dismiss behavioral risk in the general public. But the point of this study was “how should a fiduciary advisor legally obligated to act in the best interests of their clients while having legal discretion for their life savings, invest/allocate that life savings to maximize their retirement.” This isn’t about what product salespeople should sell to earn a commission, nor necessary what do-it-yoruselfers should do themselves (although that’s an interesting exploration as well).

– Michael

Okay. Did the study factor in the fiduciary’s fee and commissions on trades when comparing the S&P’s return versus the longevity annuity? Fiduciary’s don’t work for free and broker/dealers want to get paid when trades occur. I think the study would reveal much different results and favor the Longevity annuity if you subtracted 135 bps for advisory fees, etf fee, and commissions and factor tax drag of 50bps to address taxable accounts versus non-taxable. You could go even further, I would suggest most RIA’s are using mutual funds or etf’s to manage their clients accounts on top of their advisory fees, which increases the costs further. Let’s rerun the analysis using 275 bps total fees and taxes and see what happens. I think that would be a useful analysis and comparison. What do you think?

Actually, investors who diversify among low cost mutual funds, even modestly, do better than the S&P returns.

One outlier is health care. Our employer aided health insurance costs for a family of 3 rose 9% this year, certainly greater than my spouse’s annual raise. Also actuaries for companies who provide long-term care weren’t prepared for people to slash their budgets to hang onto their polices. They have asked – and in many states- succeeded in greatly hiking premiums.

Personal experience: a parent lived well into her 90s. When she needed long-term care Medicaid options were very limited. That is the norm, Luckily for her, she and her spouse worked hard, lived frugally, and built a solid asset base. Even so, her savings were at great risk. Food, clothing utilities, her home…all remained affordable. But health care costs were staggering.

I guess what we need is a diversified annuity investment similar to a defined maturity bond ETF. It’s probably already in the works.

Michael, I’ve been unable to actually identify any carriers or products that resemble the product you describe. Any ideas?

Ken,

Different companies have different labels for these. Longevity annuities, deferred income annuities (DIAs). Some only sell them inside of IRAs and call them QLACs.

Available carriers include New York Life, Mass Mutual, Guardian, Principal, Lincoln, and American General.

– Michael

Great article! But my concern is a resurgence of double-digit inflation like in the 70s. If that happens between now and when my longevity insurance kicks in 20 or 30 years from now, the real value of the payments will be a tiny fraction of what they are now. While the annuity may grow at the CPI rate after it begins, no carriers seem to offer a policy which allows for CPI-based growth prior to the first payment. So I’m left guessing at inflation, and if I guess wrong, counting on my longevity insurance to bail me out once I spend through my remaining assets, it could prove next-to-worthless. Any solution?

There is no annuity on earth that solves for hyper inflation, so no, there is no solution to this scenario. Among other things, annuities force you to make a bet against hyper-inflation. Doesn’t mean it has no place in a retirement plan, just means it’s a risk you have to consider.

Hi Michael,

I am 63, my wife is 67, and I plan to retire at age 70. I looked into longevity insurance for both of us (starting at my age 85) via Vanguard, a company I trust (I use them for most of my investments). They quoted for me on an annuity of $7,000/month starting at age 85, to the tune of $240K paid now, with payments to start 22 years from now if I live that long. That seems like an awful lot of money for an annuity that I may never even use! I figure that I can invest that $240K with some reasonable asset allocation (e.g, 50% stock/bonds, all in index funds) for the next 22 years and I’ll have that money to live on, and if I die my wife and children would have that money. If the annual stock return is 8% and the bond return 4%, that’s $936K at age 85 that I would have rather than the longevity annuity.

Am I missing something?

yes. call me and i will do an analysis that proves there is a better way. Go to free-financial-plan.com to start

Wright-Retirement.com come and get them! go to http://www.Free-Financial-Plan.com fill it out and I will blow you away with returns afterwards!